Michael has been an adjunct professor of finance at Columbia Business School since 1993 and is on the faculty of the Heilbrunn Center for Graham and Dodd Investing. In 2009, Michael received the Dean’s Award for Teaching Excellence. BusinessWeek’s Guide to the Best Business Schools (2001) highlighted Michael as one of the school’s “Outstanding Faculty,” a distinction received by only seven professors.

A: A chess match normally pits a person against another person. In freestyle chess, each player can use whatever aids they want to augment performance. Generally, the most common aid is chess-playing computer software, but you can tap other players to help you as well. So the idea is that you augment your own cognitive abilities by whatever means you can.

A: In fundamental analysis, an individual seeks to determine whether a stock (or bond, or other asset) is attractive by analyzing the so-called “fundamentals.” These fundamentals include the company’s growth prospects, position in its industry, profitability, valuation, and the quality of management. It is common for fundamental analysts to use their judgment in these assessments.

Warren Buffett, the CEO of Berkshire Hathaway and one of the richest people in the world, is probably the most famous fundamental investor.

Warren Buffett is the chairman, CEO, and largest shareholder of Berkshire Hathaway. He was the most successful investor of the 20th century and currently America’s second wealthiest person according to Forbes.

Q: What is quantitative analysis?

A: In quantitative analysis, the goal is to use algorithms to decide whether an investment is attractive. The typical process is to examine past data and determine what factors lead to outperforming the overall market or a specific benchmark. You can then let the computer identify those factors today and construct a portfolio of investments that seeks to beat the market.

Unlike fundamental analysis, there is no judgment day-to-day. The models do their thing without emotion. And that is the attraction of the approach.

Q: What can freestyle chess teach us about investing?

A: The first point that I find fascinating is that in chess, the best computer programs can beat the best humans. So there is already superhuman performance.

But what’s more interesting is that man plus machine—the freestyle teams—beat either man or machine. So for now, taking the best of humans and machines allows for better results than man or machine alone. That suggests that in chess employing a human can add value.

So that is the lesson investors can learn. Or maybe it’s better to pose it as a question: In investing, can we combine the best of what humans and computers offer and avoid the worst of each? Computers can help humans in investing because they can crunch numbers in a way that no person can. But humans can help computers by recognizing shifts in regimes that the computer won’t capture.

For now, the fundamental and quantitative cultures are largely separate. It remains to be seen whether they can merge successfully in investing as they have in chess.

Former Chess World Champion Viswanathan Anand (left) and Anson Williams, leader of Intagrand, considered the best freestyle chess team.

A: I don’t know much about what those guys are doing, but would say that some firms have been successful using these types of techniques. The best-known example is Renaissance Technologies.

James Simons, a mathematician who worked with the National Security Agency to break codes. He is the Founder and CEO of Renaissance Technologies.

Q: It is my contention that teaching freestyle chess at the scholastic level would be a very effective first step in helping student comprehend deep learning algorithms. Do you see this as a plausible assertion?

A: Absolutely. One of the advantages of having a computer program run alongside you is that it provides feedback – in effect, you get to see what moves make sense and why. And because the computer can crunch values so much faster than a human, it speeds up learning processes.

It’s interesting to note that today’s great young chess players have come of age in world where computers have always been better than humans – Kasparov lost to Deep Blue back in 1997. So young people today can learn not only from coaches and teachers but also from software programs. That is a substantial advantage versus prior generations. We saw a similar process in poker.

Benoit Mandelbrot was a Polish-born, French and American mathematician, noted for developing a “theory of roughness” and “self-similarity” in nature and the field of fractal geometry to help prove it.

Q: In your book, Think Twice: Harnessing the Power of Counterintuition, you wrote about driving Benoit Mandelbrot home after a dinner in New York City. How much has Mandelbrot’s ideas about financial markets influenced your own thinking?

A: Mandelbrot was an extraordinary polymath who was way ahead of everyone else. His work has influenced me a great deal. There’s a famous book, published in 1964 by a professor named Paul Cootner, which delved into the issue of stock market efficiency.

The term “efficiency,” borrowed from physics, measures how accurately the stock market translates inputs such as information into an output called a stock price. Markets that are efficient accurately reflect all of the information that’s out there. As a result, only new information, which is by definition random, will change stock prices. And financial economists thought that a bell-shaped distribution of price changes would be the right way to model the stock market that is largely efficient.

Mandelbrot had a paper in the book that basically said: “You guys have this all wrong.” He showed that asset price changes don’t follow a bell-shaped distribution at all. Indeed, there are huge but infrequent price moves that are very consequential but absent from the accepted model. His paper raised some eyebrows and even ruffled a few feathers, but was basically ignored by the mainstream financial economists.

Nassim Taleb, author of “The Black Swan” and “Antifragile,” considers Mandelbrot his mentor.

Q: In The (Mis)Behavior of Markets, Mandelbrot wrote:

My principal objections—that prices do not follow the bell curve and are not independent— were heeded, and hundreds of economists and market analysts have by now documented their validity. But despite recognition of the problem, the old methods have surprising staying-power. The “classical” formulae of Bachelier and his heirs—how to build an investment portfolio, to evaluate the financial value of a new factory, to judge the riskiness of a stock—remain on the curriculum at hundreds of business schools around the world and are a standard part of the Chartered Financial Analyst exams administered to thousands of young brokers and bankers. They remain part of the orthodoxy of Wall Street professionals, too.

This was written in 2004, has there been much change in the Wall Street orthodoxy in the last ten years or so?

A: As Mandelbrot said, even though he showed that prices don’t follow a bell-shaped distribution more than 50 years ago, a fact that has been confirmed over and over, the basic tools of Wall Street have not changed much. Practitioners do have modifications to the models to reflect that extreme outcomes occur from time to time. But the challenge is coming up with a model that is both empirically valid and tractable. It’s hard to do both at the same time.

Q: In

Think Twice, you also wrote about David X. Li’s Gaussian copula function being near the center of the 2007-2009 financial crisis. Li’s model is an example of what Mandelbrot described as a “classical” formula of a Bachelier’s heir that is fundamentally flawed. According to a recent

New York Times article “American banks have nearly $280 trillion of derivatives on their books.” If the same “classical” formulae still dominate financial trading, then considering the recent decrease in oil prices and decline of the Russian ruble, should people be concerned?

A: It’s important to separate a couple of issues. First, derivatives in and of themselves need not be dangerous. There are plenty of derivative contracts that are plain vanilla and that play an important role in commerce. For example, farmers may use derivatives to hedge the value of their crops. Nothing untoward there.

The second issue is with something like the Gaussian copula function. One of the original uses of the function was to determine the likelihood that a husband or wife would die following the death of their spouse. So it measures the likelihood of more than one bad thing happening. And in the case of a second spouse dying after the death of the first one, there are actuarial data that provide some guidance. By the way, husbands are more likely to die shortly after the death of their wives than the other way around.

The problem arose when the copula function was applied to financial instruments in an inappropriate way. Now the question wasn’t about the death of spouses, but rather the default of bonds or mortgages. The beauty of the copula function was that it provided a single number to represent the risk of cascading failure. The problem was that it was not up to the task, so investors made inappropriate bets.

So I don’t have any particular insight into today’s situation, but would say that the issue a few years back was not the presence of derivatives per se but rather some of the ways they were used.

David Li with his statistical formula for modeling the behaviour of several correlated risks at once. Li is currently an Investment Manager at AIG Investments.

Q: In your book, The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing, you say that it “was pure luck” that you got your job at Drexel Burnham Lambert. You also tell the Henny Youngman joke that whenever someone asked, “How’s your wife?” he’d reply, “Compared to what?” Compared to the success of Bill Gates or Warren Buffett, you may not seem very lucky. How does one assess if an event is lucky or unlucky?

A: This is an important question, and the answer hinges a lot on how you define luck. I spent a lot of time researching this question, and settled on a definition from the philosopher, Nicholas Rescher. He basically said luck exists when three conditions are in place: 1. It happens to you or your organization; 2. It can be good or bad; and 3. It is reasonable to expect that a different outcome could have occurred.

Now when you examine the Bill Gates’s or Warren Buffett’s of the world, you can confidently say they benefited from great skill and great luck—indeed, this is true for all positive outliers.

But to answer the question, applying the definition can help you think about luck’s role in particular outcomes.

Q: In addition,

The Success Equation tells the story of software pioneers Gary Kildall. A Businessweek article called Kildall “

The Man Who Could Have Been Bill Gates.” Kildall sold his company to Novell for $120 million, was he unlucky?

A: I don’t think Kildall was unlucky, no. But the point of that story is that he was put into a position to do the deal with IBM that Bill Gates eventually did. He clearly didn’t see the opportunity the way that Gates did, and Gates deserves all the credit in the world for doing what he did. But it’s not hard to imagine a scenario where Kildall played his cards differently and the outcome of the world would be quite different.

Now I’m confident that Bill Gates would have been a very successful guy in almost any scenario you can come up with. But it’s also likely that he wouldn’t be the richest guy in the world.

What would the world look like if Bill Gates didn’t make that deal with IBM?

Q: Your book also tells the story of Deanna Brooks, Playmate of the Month in May 1998, who picked stocks that performed better than 90 percent managers who actively try to outperform a given index. What does this tell us about the investing profession?

A: It tells you that picking stocks that beat the market is really hard. It also tells you that there is a lot of luck in stock picking. Not all luck, but a lot of luck.

I think the key insight is why it’s so hard. The answer is not that investors aren’t skillful. By any objective measure, investors have never been more skillful. The answer is that stock prices do a good job of reflecting the information that’s out there. So the skill of investors is reflected in prices leaving more to luck.

There’s a great little test, which I learned from the poker community, to determine whether there’s any skill in an activity: ask if you can lose on purpose. If can lose on purpose, there must be skill. Investing is interesting in that it’s hard to win, or lose, on purpose.

Deanna Brooks, my next investment consultant.

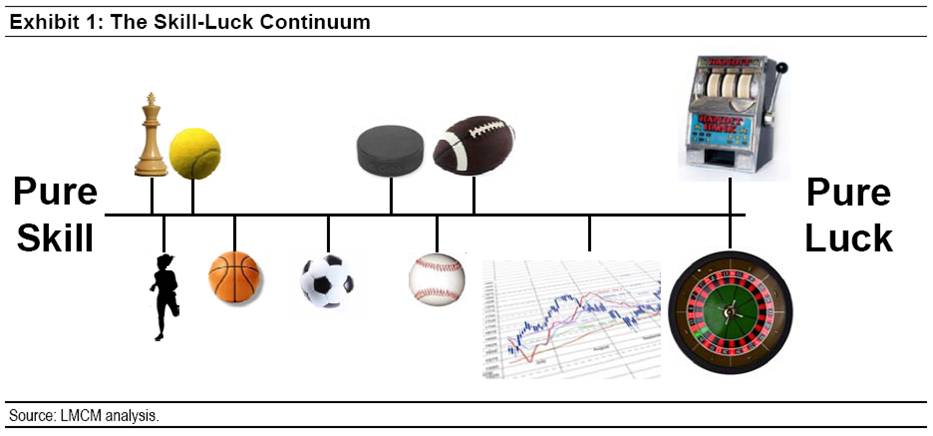

Q: You developed a table comparing the contribution of luck in professional sports leagues. What does it mean to say that the contribution of luck in the NBA is 12% and in the NFL it’s 38%?

A: The full answer to this is a little technical, but let me come at it this way: The question we ask is, “What would we expect if the outcomes of each game were determined by luck alone, and how far from that expectation are the real outcomes?”

So if luck alone determined the outcome, we could model each game as a coin toss. The captains of each team meet in the middle of the court or field, the ref flips a coin, one player calls heads or tails, and based on that outcome alone everyone hits the showers and goes home.

Well, we know what that model looks like—it’s a binomial distribution. And we know that the actual outcomes are from playing he games for a season. So by comparing the actual outcomes to the luck model, we can assess the contributions of skill and luck. Again, the method in the book uses some fancier methods from statistics, but that is the idea.

Q: If we fielded a sports team of Playmate, it would be hard to find a high school that they could beat, let alone a professional team. Is the “luck” of investing and the “luck” of professional sports leagues actually the same thing?

A: It is. But you’re highlighting a very important point. This luck-skill framework is more about capturing the relative differences in skill than the absolute level of skill. In other words, you might have two very skilled teams playing one another, but if their skill levels are equal the outcome will be largely the product of luck. Again, their skill is offsetting.

Now in the case of the stock market, the relative differences in skill are small because the stock market itself embeds a ton of skill. But in the case of sports, it’s easy to see that there would be differential skill. That’s why a Playmate, who was lucky, can do well for a year but why a team of Playmates playing a sport would be unable to beat a skillful team.

I could be wrong. In the name of science I am willing to test this hypothesis.

Q: You wrote:

Many organizations, including businesses and sports teams, try to improve their performance by hiring a star from another organization…. But the people who do this type of hiring rarely consider the degree to which the star’s success was the result of either good luck or the structure and support of the organization where he or she worked before. Attributing success to an individual makes for good narrative, but it fails to take into account how much of the skill is unique to the star and is therefore portable.

Was this a factor in you returning to Credit Suisse?

A: You’d have to ask my boss!

The serious point is that we often misattribute performance to the individual when we should understand the context within which he or she operates. The work in this area is quite compelling: stars very often lose their luster as they switch organizations. Part of it may be simple reversion toward the mean—in other words, they had gotten lucky before and their luck runs out—and part of it is environmental.

Daniel Kahneman is a psychologist notable for his work on the psychology of judgment and decision-making, as well as behavioral economics, for which he was awarded the 2002 Nobel Memorial Prize in Economic Sciences. His empirical findings challenge the assumption of human rationality prevailing in modern economic theory.

Q: You also quoted Melissa Finucane and Christina Gullion about the keys to competent decision making:

[U]nderstanding information, integrating information in an internally consistent manner, identifying the relevance of the information in a decision process, and inhibiting impulsive responding.

A: I view these are somewhat different concepts. I would say that the quote from Finucane and Gullion relates more to what Daniel Kahneman calls System 1 and System 2 thinking. System 1 is experiential. It is fast, automatic, and difficult to train. System 2 is analytical. Is it slow, purposeful, and malleable. Good decision making, especially in complex settings, requires use of System 2 thinking more than we would like. We all tend to be cognitively lazy, and let System 1 do most of the deciding.

The discussion in “three steps” is really about the theory of theory building. Most people shun the word “theory” because they equate it to “theoretical,” which connotes impracticability. But theory is really an explanation of cause and effect – so good theory is incredibly practical. So it’s a good idea, in the world of business, investing, or sports, to ask whether the theories you adhere to can be improved. In many cases they can, and the three step process helps illuminate the path to improvement.

Q: Thank you Michael Mauboussin for your time. Is there anything else that you would like people to know?

A: Nothing else for me to add but thanks to you, Terrance!

Awesome piece of writing. Thanks so much for sharing.